In a collaborative effort led by the National Association of Insurance Commissioners (NAIC), state insurance regulators have launched a nationwide Property & Casualty Market Intelligence Data Call (PCMI).

This move, aimed at collecting and analyzing data from over 80% of the U.S. property insurance market, marks a significant step toward enhancing transparency, accountability, and resilience within the industry.

What is the PCMI Data Call?

At its core, the PCMI Data Call is more than just a request for information. It’s a comprehensive effort to understand the dynamics of the property and casualty insurance market in the face of escalating natural disasters, rising reinsurance costs, and inflationary pressures.

By gathering data from more than 400 property insurers across the nation, regulators aim to gain insights into market costs, coverages, protection gaps, and more. This initiative underscores the critical role of state insurance regulators in protecting consumers, ensuring fair competition, and fostering healthy insurance markets.

Why This Matters to Insurers

For insurance companies, the implications of this data call are profound. The demand for detailed, ZIP-code-level data on premiums, policies, claims, and other aspects introduces both challenges and opportunities.

Insurers must comply with these new regulatory requirements and use the opportunity to leverage insights gained to improve their products, pricing, and overall market strategies. Amidst these complexities, the need for efficient, reliable data management and analytics tools becomes evident.

A Modern Data Management Platform: Empowering Insurers in Regulatory Compliance and Beyond

In the rapidly evolving landscape of insurance regulation, the advent of the PCMI Data Call indicates a pressing need for insurers to adapt to regulatory changes through innovative data use. Through this regulation, there is also an opportunity for insurers to leverage detailed, ZIP-code-level data to significantly enhance underwriting processes and claims management.

To successfully meet these new demands – as well as any other new regulations that may arise in the near future, insurers need to rethink their approach to data management and analytics fundamentally.

These advancements could be supported by new data reports and dashboards, i.e. an underwriting exposure management report, and CAT (Catastrophic) claims approaches, alongside CAT reporting and Non-CAT reporting.

Let’s take the underwriting exposure management reports for example. This report would aim to address a fundamental challenge in insurance – the geographic distribution of risk. By applying filters such as State, County, City, ZIP, Service Industry Codes, Line of Business, and product, insurers can gain insights into Total Insured Value (TIV) for building, contents, and business interruption, in addition to written premium values.

This strategic approach ensures a diversified risk portfolio, avoiding overconcentration in specific geographic areas and thus enhancing the stability of the insurance pool.

On the claims side, the distinction between CAT reporting and non-CAT reporting emerges as a critical tool. This differentiation allows insurers to match claims coverage more accurately with written premiums and incurred losses, including reserves, payments, and recoveries. The built-in traceability and lineage provide the actuarial data needed to refine pricing rates accurately. Furthermore, coverage match capabilities enable the calculation of Loss Ratios at the most detailed coverage level, offering unparalleled precision in claims management.

Such reporting capabilities not only equip insurers to meet current regulatory demands like the PCMI Data Call but also pave the way for future readiness in an increasingly complex regulatory environment. By adopting these advanced data analytics and reporting methodologies, insurers can transform regulatory compliance into an opportunity for strategic improvement, ensuring operational efficiency and competitive advantage in a market that champions agility and informed decision-making.

The key lies in adopting a holistic, forward-thinking strategy that positions them not just for compliance, but for competitive advantage and market innovation.

Attributes of a Modern Data Management Platform

To adeptly respond to regulatory demands like the PCMI Data Call, insurers should focus on several critical attributes in a data management platform.

First and foremost, data curation and accessibility are paramount. Insurers need a system where data is not only centralized, but has undergone a rigorous curation process. This ensures that the data is clean, consistent, and ready for analysis or reporting at a moment’s notice.

Another essential feature is built-in traceability and governance tools. With increasingly stringent regulatory requirements, insurers must be able to demonstrate the integrity and lineage of their data. This requires tools that can automatically document data movements and transformations, creating a transparent audit trail.

Flexibility and scalability also come into play. The right platform can handle varying volumes of data and adapt to changing regulatory landscapes without requiring insurers to undertake significant overhauls or disruptions to existing processes.

Lastly, the data management platform should enhance operational efficiency. This means providing low-code or no-code tools that enable insurers to rapidly build and configure reports and dashboards with ease. Some data management systems for insurers also feature regulatory compliance modules to help insurers stay compliant with ease and focus on other business aspects. By significantly reducing the time and technical expertise needed to extract insights, insurers can more quickly respond to regulatory requirements and market changes.

Elevating Compliance to Strategic Opportunity

By focusing on these attributes, insurers can turn regulatory compliance from a checkbox exercise into a strategic asset. Beyond merely collecting and reporting data, a modern data management platform should enable insurers to unearth insights that drive smarter underwriting decisions, more targeted customer relationships, and innovative product development.

In this way, meeting the PCMI Data Call and other regulatory demands becomes an opportunity to not only reaffirm commitment to transparency and accountability but also to reinforce a culture of data-driven decision-making. This culture positions insurers to lead in a market that values agility, foresight, and resilience.

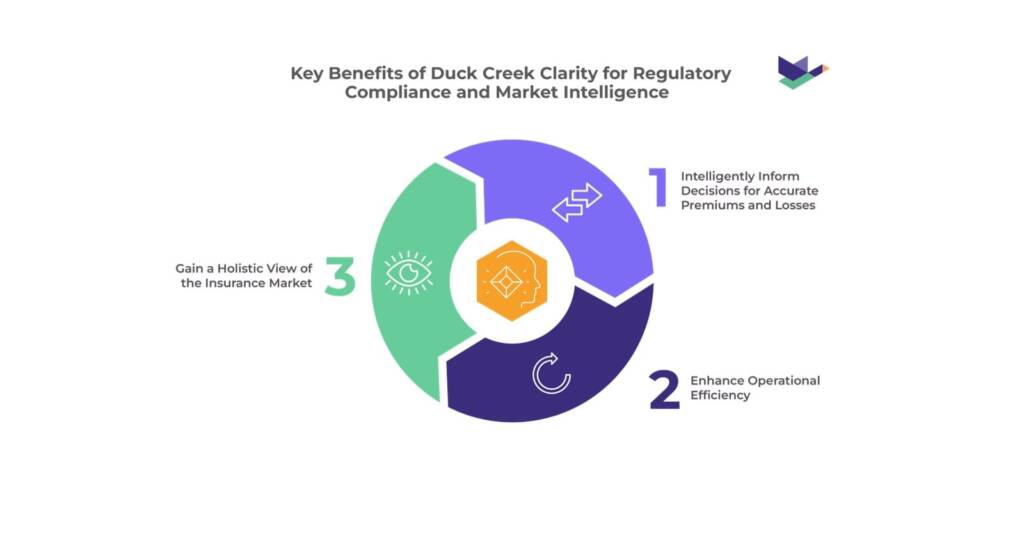

Duck Creek Clarity is a solution designed to address the very challenges posed by the PCMI Data Call and others like it. Duck Creek Clarity offers insurers a cloud-native data management, reporting, and analytics platform that simplifies the collection, analysis, and utilization of vast amounts of data.

With features like curated data centralized in Snowflake, pre-built Microsoft Power BI Reports, and low-code tools for configuring business intelligence dashboards, Duck Creek Clarity stands as an invaluable asset for insurers navigating the changing regulatory landscape. Learn more about Duck Creek Clarity here.

Moving Ahead with New Regulations

The Property & Casualty Market Intelligence Data Call represents a significant moment for the U.S. property insurance market.

As insurers work to comply with this and future regulatory initiatives, Duck Creek Clarity offers a pathway to not just meet these demands, but to transform them into opportunities for strategic growth and market leadership.

By leveraging Duck Creek Clarity, insurers can ensure that they are always ready for change and be able to thrive in an ever-evolving regulatory environment.